May 28, 2026

By Brian Bastian, Head of Product

When the Palisades and Eaton fires tore through Los Angeles in January 2025, they left behind a landscape of striking contrasts. Some neighborhoods were reduced to ash. Others, just blocks away, survived largely intact. The fires burned intensely through certain corridors, then eased as they crossed into different terrain.

A new study published in AGU Advances in May 2026 offers a rigorous scientific explanation for those patterns — and it has important operational implications for anyone responsible for managing commercial property exposure in wildfire-prone areas.

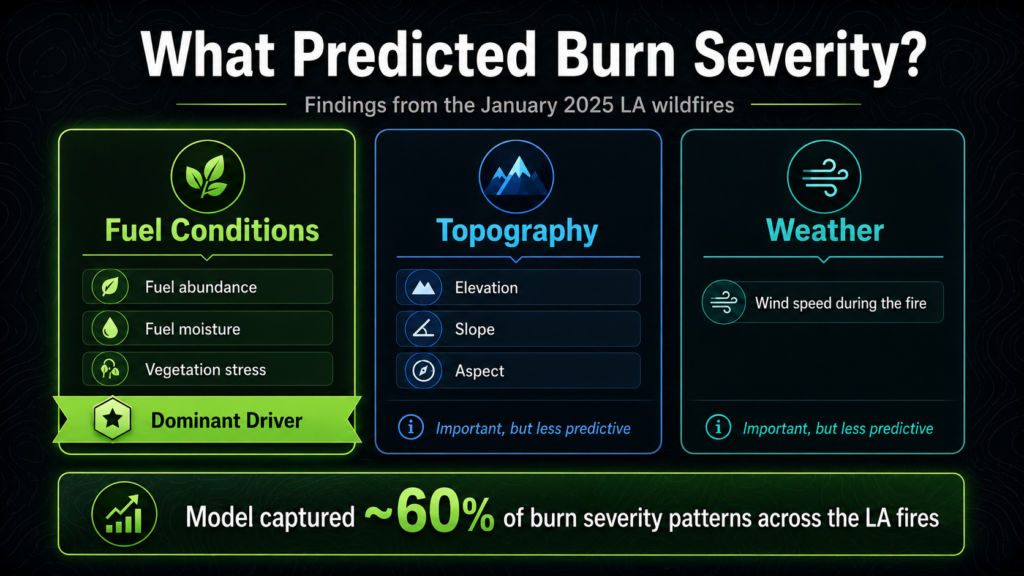

Researchers analyzed all three major January 2025 LA wildfires using pre-fire satellite data, building a predictive model of burn severity. Their finding: the state of the vegetation before the fire started was the dominant driver of how severely any given area burned — more so than slope, elevation, or wind speed during the event. Using satellite instruments that measure plant stress and moisture, the model predicted burn severity patterns with approximately 60% accuracy.

For underwriters and risk managers, the practical message here is not about adjusting prices mid-policy or chasing dynamic data. Underwriting takes a long-term view — policies are written for 12-month terms, and risk decisions are made at the time of binding. The value of this research lies elsewhere: it tells us what to look for when assessing a risk, what operational protocols should be in place during a policy year, and when and how to engage policyholders to drive the mitigation actions that actually reduce loss.

What the Research Found

The study used data from two NASA satellite instruments — ECOSTRESS, which measures plant temperature and water stress, and EMIT, which maps surface minerals and vegetation characteristics — to characterize fuel conditions across the burned areas before the fires began.

When researchers fed these pre-fire fuel measurements into a random forest regression model alongside topographic variables (slope, elevation, aspect) and weather data (wind speed), fuel conditions emerged as the clear primary driver of burn severity. The model captured roughly 60% of burn severity variation — a meaningful result for a complex physical phenomenon, and one that held up particularly well in the shrub- and scrub-dominated wildland-urban interface terrain that characterizes much of Southern California.

The practical translation: how dry, stressed, and abundant the vegetation is in the weeks and months leading into a fire season has more influence on loss outcomes than the specific weather on the day the fire occurs. That’s a significant finding, because fuel conditions are something that can be managed. Wind is not.

The Underwriting Takeaway: Ask Better Questions at Submission

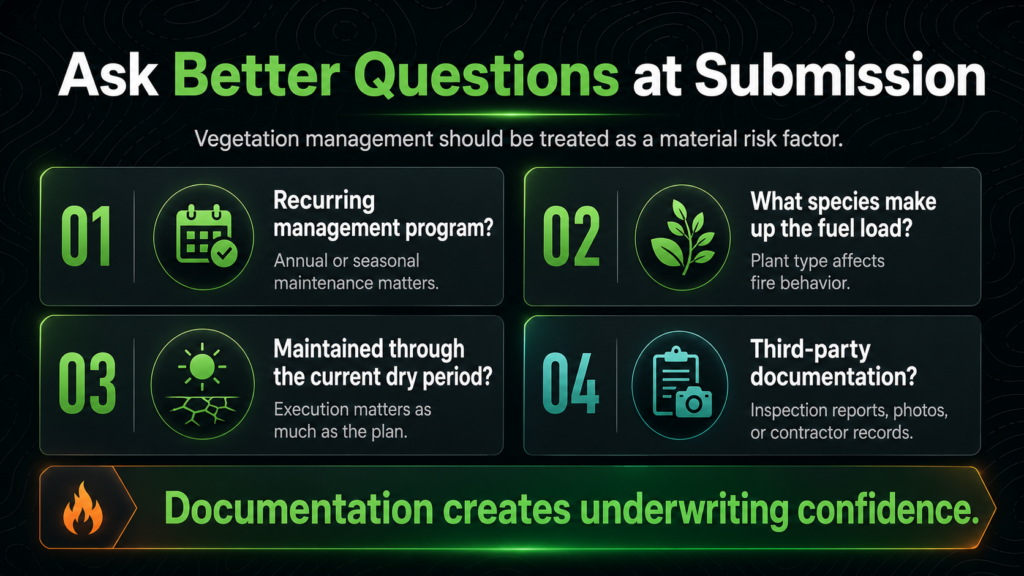

For commercial property underwriters, this research reinforces something that often gets underweighted at submission: whether a property has an active, documented vegetation management program is a material risk factor — not a nice-to-have or a simple checkbox.

A documented vegetation management program is a material risk factor — not a nice-to-have or a simple checkbox.

The standard questions about defensible space distance are a start, but the science suggests the questions need to go deeper:

- Is there a written, recurring vegetation management program? A single clearing done at property acquisition doesn’t tell you much about current conditions. Annual or seasonal programs do.

- What species make up the fuel load? Native, fire-adapted, drought-tolerant plantings behave very differently than overgrown ornamental landscaping or invasive dry grasses at the perimeter.

- Has the program been maintained through the current drought or dry period? A management plan is only as good as its execution. Vegetation that was green and managed at last renewal may be dry and overgrown today.

- Is there third-party documentation? Inspection reports, photos, contractor records, or participation in a recognized program (e.g., IBHS Wildfire Prepared Home/Business, Firewise USA) provide much more underwriting confidence than self-reported answers.

These questions matter because the science now directly supports the claim: documented fuel management reduces the severity of burn outcomes at the property level. That’s defensible in the underwriting file, and it’s the kind of risk differentiation that supports better placement decisions.

Active Event Management: Using Fuel Conditions as an Operational Trigger

One of the more actionable implications of this research isn’t about underwriting at all — it’s about what happens during the policy year, particularly in the weeks surrounding peak fire weather.

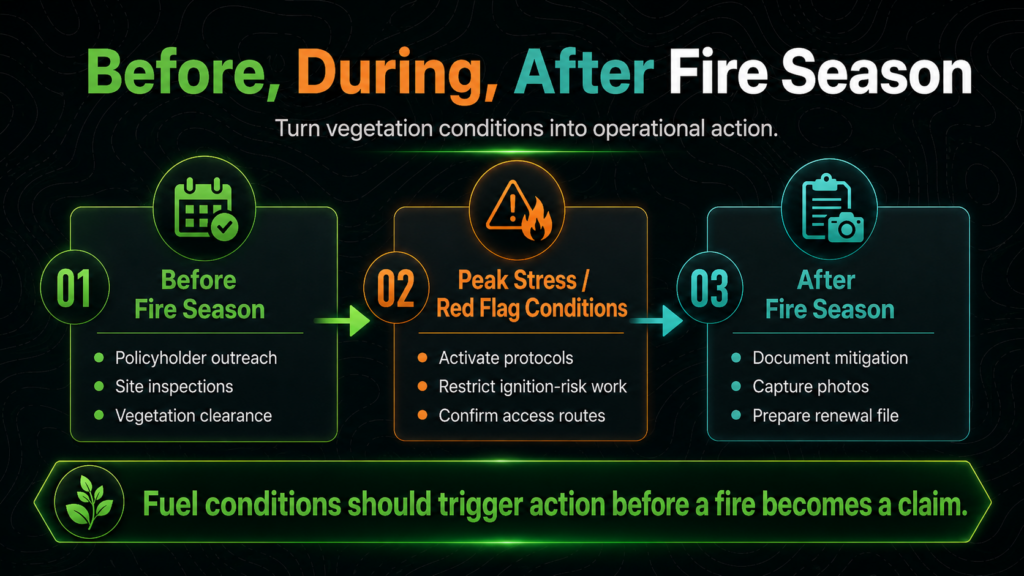

If pre-fire fuel conditions are the primary driver of burn severity, then the period of peak vegetation stress — typically late summer through fall in California and the Mountain West — is the critical window for operational action. This is when risk managers and their carriers should be most engaged with commercial property policyholders.

That engagement can take several forms:

- Pre-season policyholder communications. Before fire season begins — typically June for Southern California, July/August for Northern California and the Mountain West — carriers and risk managers can proactively reach out to commercial policyholders in high-exposure areas with specific, actionable guidance: vegetation clearance reminders, ember-resistant vent covers, property inspection checklists. Framed correctly, this isn’t administrative overhead; it’s loss prevention intelligence delivered at the highest-leverage moment.

- Just-in-time mitigation triggers. When extended drought conditions, heat events, or fire weather watches are forecast, that’s the signal to mobilize. Commercial property operators should have pre-established protocols for their facilities in fire-prone areas: crew scheduling for fuel reduction, site inspections, confirmation that defensible space has been maintained, and communication trees in place with local fire authorities. Risk managers can use seasonal drought and vegetation stress indicators — many of which are publicly available through USFS, USGS, and state fire agencies — to trigger these protocols.

- Active event management during Red Flag conditions. When Red Flag Warnings or Fire Weather Watches are issued — the official NWS designation for conditions of low humidity, high winds, and dry fuels — commercial property operators should activate event protocols immediately: postponing or halting any ignition-risk operations (grinding, welding, mowing dry grass), confirming site-level contacts are in place, and ensuring emergency access routes are clear. The research suggests that properties entering Red Flag conditions with already-stressed, dry fuel loads are at significantly higher loss potential than those that are well-managed.

- Post-season documentation. After fire season, documenting what mitigation was done during the policy year — and what conditions looked like at key risk windows — creates a record that is genuinely useful at renewal. It demonstrates active stewardship and provides the underwriter with evidence that the risk was managed, not just assessed.

The Commercial Property Dimension

Commercial properties introduce layers of complexity that make the vegetation management question more consequential than it is for a single-family home. A warehouse, distribution center, multi-family complex, or hospitality property in the wildland-urban interface may have:

- Large parcels with extended perimeters that are difficult to monitor and manage consistently

- Third-party tenants or operators who may not be aware of or invested in fire mitigation protocols

- Operational activities (equipment, vehicles, stored materials) that can complicate evacuation and increase ignition risk

- Business interruption exposure that can dwarf the physical property loss — especially relevant for hospitality, healthcare, or industrial facilities with specialized equipment or operations

The research finding — that fuel conditions at the site level are the primary loss driver — makes a strong case for commercial property risk managers treating vegetation management as a named line item in their annual risk management budget, not an afterthought. The ROI on fuel management, when measured against the potential severity reduction in a fire event, is compelling. And the documentation of that investment is increasingly valuable in a market where carrier appetite for wildfire-exposed commercial risks is shrinking.

What Property Owners and Risk Managers Should Do Now

Translating this research into practice doesn’t require new technology or complex modeling. It requires operational discipline:

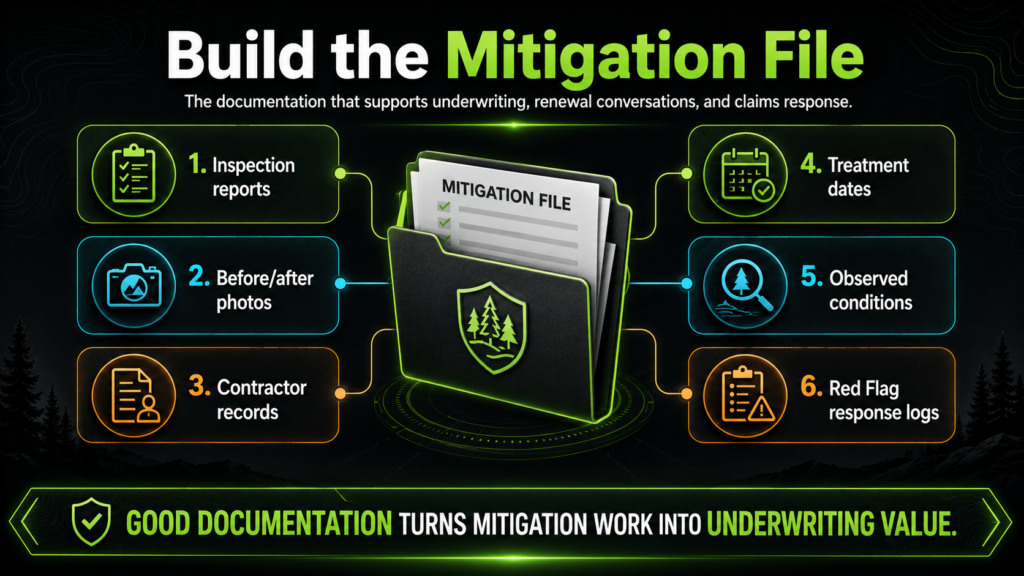

- Build a pre-season vegetation management checklist specific to each property. Not a generic one-size-fits-all document — a checklist that reflects the actual site conditions, species present, and proximity to wildland fuels. Have it inspected and signed off before June 1 in California; before July 1 in the Mountain West.

- Establish a Red Flag response protocol and make sure site personnel know it. This should be as automatic as a severe weather protocol — triggered by the NWS designation, not by waiting to see what happens. It should include operations restrictions, a notification tree, and a site inspection step.

- Keep a running log of vegetation management activities. Dates, contractors used, areas treated, conditions observed. This is your underwriting documentation at renewal and your claim support file if the worst happens.

- Work with your insurance advisor to understand how your carrier views documented mitigation. In an increasingly constrained wildfire market, carriers with appetite for well-managed commercial risks will differentiate on this. The documentation of an active management program can be a meaningful factor in placement and terms.

How Property Guardian Can Help

Property Guardian works with commercial property owners, risk managers, and their underwriters to conduct site-specific wildfire risk assessments that go well beyond proximity models. We evaluate actual fuel conditions, management practices, structure-level vulnerabilities, and site-specific ignition pathways — and we help clients build the operational protocols and documentation that serve them at the underwriting table and in the event of a loss.

The vegetation on and around your property before a fire starts is the most important variable in determining how bad that fire will be for you.

For clients who need active intelligence when it matters most, our Overwatch product provides real-time wildfire event monitoring, automated alerts, and structured response support for commercial property portfolios. When a fire ignites near an insured or managed property — or when Red Flag conditions escalate into an active threat — Overwatch delivers timely, property-specific intelligence so risk managers and their clients can act quickly and decisively. It bridges the gap between pre-season risk assessment and in-event response: knowing your exposure before fire season begins is essential; knowing exactly what is happening at your specific properties when a fire is burning is what drives the response that protects people, operations, and assets.

The science is clear: the vegetation on and around your property before a fire starts is the most important variable in determining how bad that fire will be for you. Managing that variable — systematically, documentably, and year-round — is the most direct investment a commercial property owner can make in wildfire resilience. And when fire does come, Overwatch ensures that risk managers and property owners aren’t waiting on news reports — they’re receiving the property-level intelligence they need to respond.

Sources

AGU Advances study summary, Eos / Maven’s Notebook (May 2026): Want to Predict Wildfire Severity? Look to the State of Vegetation

Phys.org (May 2026): Want to predict wildfire severity? Research says look to the state of vegetation

Maven’s Notebook summary (May 6, 2026): EOS: Want to predict wildfire severity? Look to the state of vegetation