July 7, 2026

By Brian Bastian, Head of Product

Sixty-one percent of the Lower 48 states are currently sitting in moderate to exceptional drought, according to the U.S. Drought Monitor, with two-thirds of the West under severe stress heading into what forecasters expect to be one of the more destructive wildfire seasons in years. AccuWeather’s 2026 outlook calls for 65,000 to 80,000 fires and 5.5 to 8 million acres burned nationally, with fewer total fires but larger, harder-to-contain ones. Federal fire agencies are already flagging above-normal significant fire potential for the Southwest, California, the Great Basin, the Rockies, and the Northwest through August.

None of that is the part commercial property risk managers should be most worried about right now. The part that deserves attention is quieter, and it lives inside the fine print of business interruption and civil authority coverage that most teams have never had reason to test.

Why Evacuation Practice Has Outpaced Policy Language

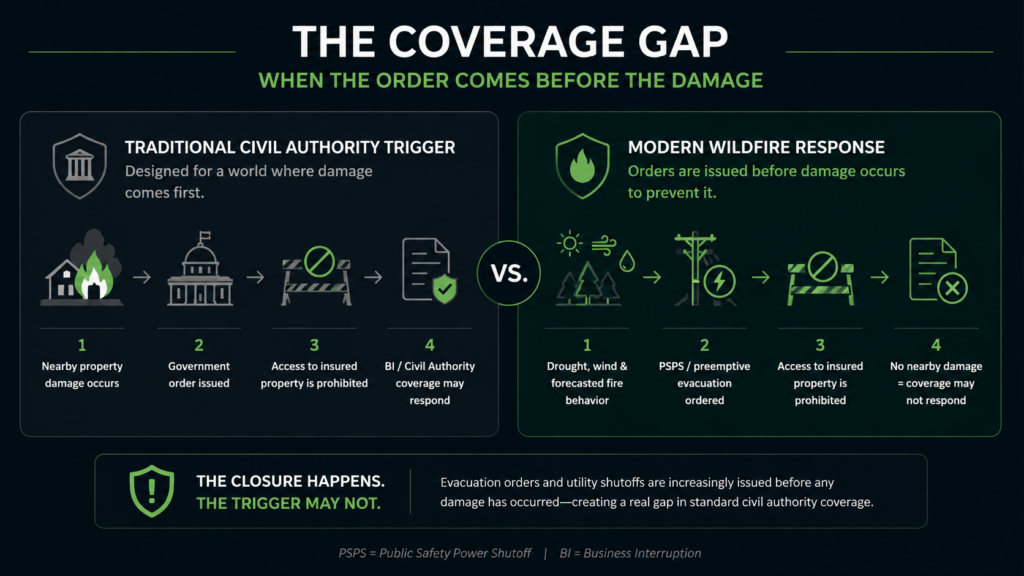

Civil authority coverage, the piece of a business interruption policy that responds when a government order blocks access to an insured property, was written for a fire pattern that no longer describes how many evacuations actually happen. The classic trigger requires two things: an order prohibiting access to the property, and that order being caused by damage to property other than the insured premises from a covered peril. In practice, that has usually meant a nearby fire has already caused physical damage before the order goes out, and even then coverage typically carries a waiting period of around 72 hours and is capped at two to four weeks or subject to a sublimit.

“Civil authority coverage was written for a fire pattern that no longer describes how many evacuations actually happen.”

The problem in 2026 is that evacuation orders are increasingly issued before any damage has occurred at all. Utilities are calling Public Safety Power Shutoffs during high-wind, high-drought conditions to prevent their equipment from sparking a fire in the first place. Fire agencies are ordering preemptive evacuations based on fire behavior forecasts and drought-driven fuel conditions rather than waiting for flames to reach a community. Both practices make enormous sense from a public safety standpoint. Both also create a real possibility that a business closed by a precautionary order will find its civil authority coverage does not respond, because the policy’s damage-to-nearby-property trigger was never satisfied.

This is not a hypothetical for anyone with property in a wildland-urban interface zone, near utility infrastructure subject to shutoff protocols, or downwind of federal and state land where fire agencies have broad authority to close access preemptively. It is a gap that widens every time drought conditions push fire behavior further ahead of the assumptions built into standard policy language decades ago.

What This Means for Commercial Property Teams

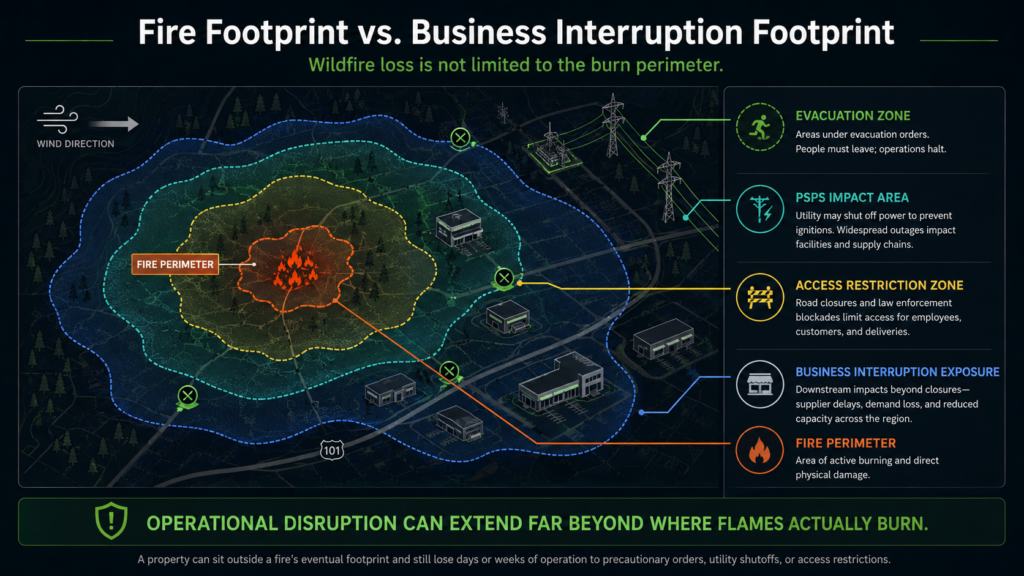

For a facilities leader or corporate risk manager, the operational impact of a multi-day access closure looks the same whether it was triggered by an actual fire perimeter or a precautionary shutoff. Payroll still runs. Perishable inventory still spoils. Tenants still expect rent relief conversations. Supply chains still stall. The financial exposure does not care why the order was issued. The insurance policy, unfortunately, often does.

Commercial property teams that assume “if a wildfire closes us down, our BI policy covers it” are working from an outdated picture of how modern wildfire response actually unfolds. The gap is most acute for properties that have never filed a civil authority claim before, since the first time a team discovers how narrowly the trigger language is drawn is often in the middle of an actual closure, when there is no time left to negotiate better terms.

Practical Takeaways for Underwriters and Risk Managers

A few steps are worth taking before, not during, peak fire season.

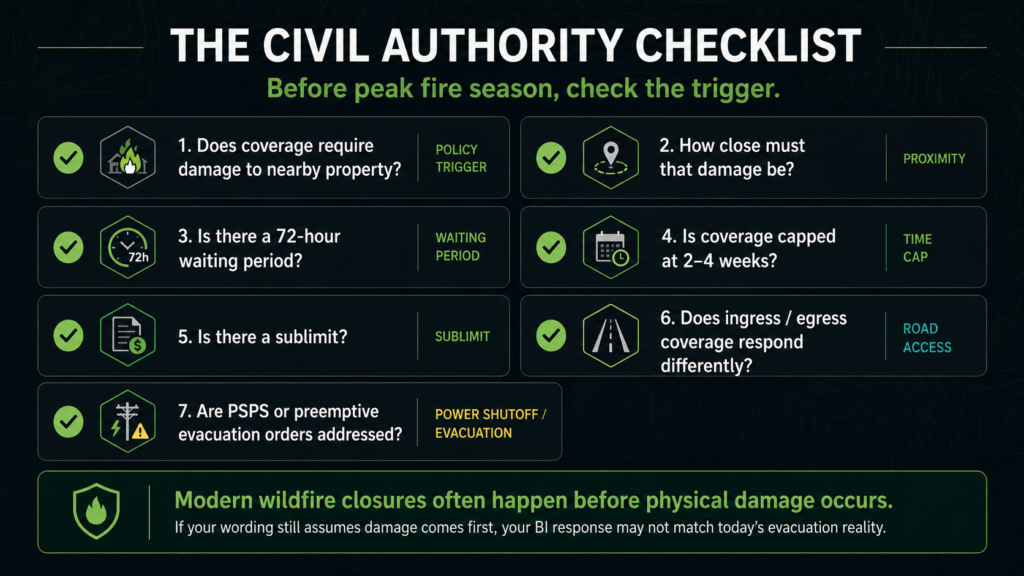

Review the actual civil authority and ingress/egress language in current policies, specifically the proximity-of-damage requirement, the waiting period, and any sublimit. Many policies were bound years ago under different assumptions about how evacuations get triggered, and renewal season is the natural point to renegotiate terms that better reflect how orders are actually issued today.

Map exposure to preemptive evacuation and Public Safety Power Shutoff (PSPS) zones separately from wildfire perimeter risk. A property can sit well outside a fire’s eventual footprint and still lose weeks of operation to a precautionary order. Portfolio-level views that account for utility shutoff protocols and evacuation zone overlays, not just historical fire recurrence, give a more accurate picture of where business interruption exposure actually concentrates.

Talk to brokers now about parametric or non-damage business interruption options that respond to the fact of a closure order rather than requiring proof of nearby physical damage. These products exist precisely because standard civil authority language has not kept pace with how wildfire response has changed.

Build continuity plans that assume closures will run longer than they used to. With fewer, larger fires expected this season, access restrictions in affected regions are likely to last longer than the two-to-four-week caps many BI policies were designed around.

The properties and portfolios that come through this wildfire season with the least financial disruption will be the ones whose teams understood their actual exposure before an evacuation order arrived, not after. Property Guardian’s active wildfire intelligence gives commercial property and risk teams real-time visibility into fire behavior, evacuation zones, and threat status around their properties as events unfold, so decisions about continuity, communication, and documentation can be made with facts on the ground rather than after the fact.

Sources

National Interagency Coordination Center: North American Seasonal Fire Assessment and Outlook

National Interagency Coordination Center: August 1, 2026 Outlook Period

Drought.gov: National Significant Wildland Fire Potential Outlook