April 30, 2026

By Brian Bastian, Head of Product

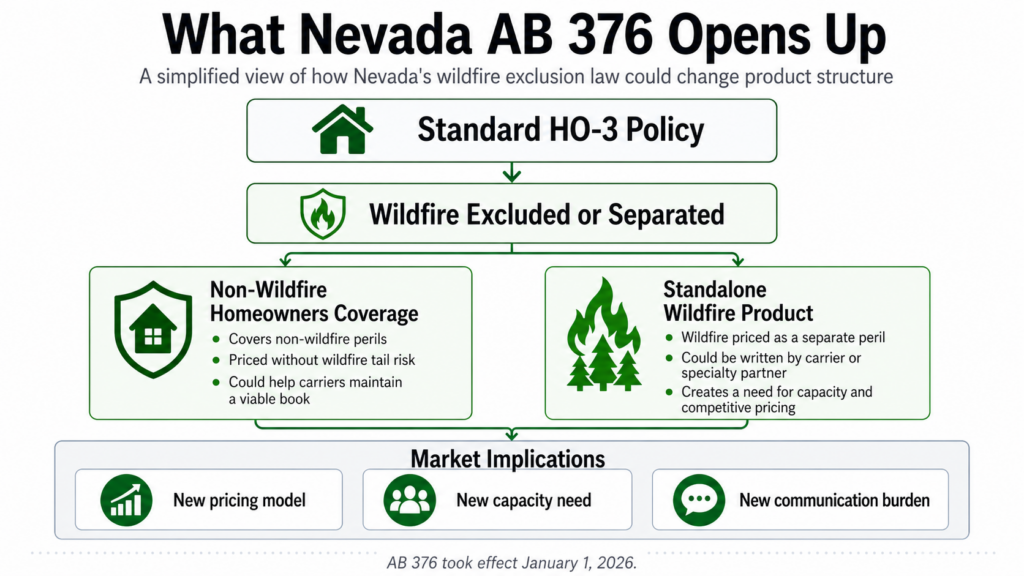

Nevada is the first state in the country to explicitly permit property insurers to exclude wildfire coverage from standard homeowners policies. Assembly Bill 376, signed into law in June 2025 and effective January 1, 2026, gives carriers two options: separate wildfire as a standalone, separately priced product, or remove it from policies altogether.

The law passed with broad bipartisan support and was framed as a four-year regulatory sandbox, designed to give admitted carriers enough flexibility to stay in the market rather than exit. The legislature’s diagnosis was straightforward. Carrier withdrawals driven by wildfire liability had already caused policy cancellations and non-renewals in Nevada to surge to nearly 158,000 in 2023 alone. Something had to give.

But the implications of AB 376 extend well beyond Nevada’s borders. Every carrier, MGA, and reinsurer with western property exposure should be paying close attention, because Nevada has just run an experiment that other state legislatures and regulators are watching closely.

What the Law Actually Opens Up

For carriers, AB 376 creates an explicit legal framework to do something they have long wanted: price wildfire risk as a discrete, separable peril rather than absorbing it into an all-perils homeowners product where cross-subsidization has made the math increasingly difficult.

The structure this enables is notable. A carrier could write a standard HO-3 that excludes wildfire, price that product on non-wildfire perils, and maintain a viable book in Nevada without carrying wildfire tail risk on every policy. A separate wildfire-specific product, written by the same carrier or a specialty partner, could then be offered to policyholders who want that coverage. The risk, the pricing, and the capital treatment for each peril would be independent.

For MGAs and specialty programs with wildfire expertise, this is a potential market opening. If admitted carriers exercise the exclusion, there is a coverage gap that someone will need to fill. The question is whether the standalone wildfire product market develops fast enough, and with sufficient capacity and competitive pricing, to actually serve Nevada policyholders before the gap becomes a consumer protection crisis.

The Structural Problem No One Has Solved Yet

Here is where the Nevada situation gets complicated, and where carriers need to think carefully before simply celebrating the new flexibility.

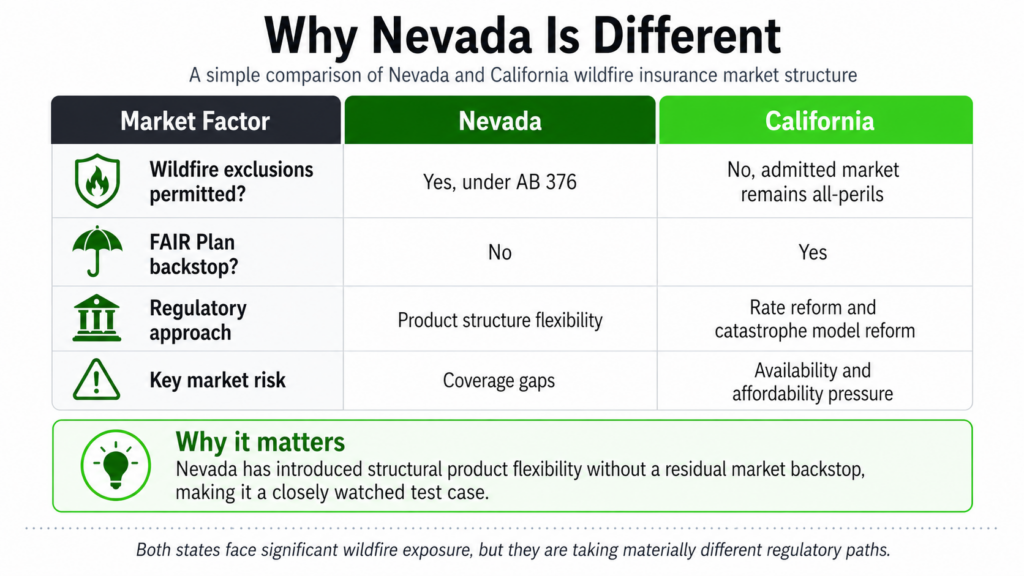

Unlike California, Nevada has no FAIR Plan. There is no state-backed residual market mechanism providing a coverage floor if admitted carriers exercise the wildfire exclusion and the E&S market fails to adequately fill the gap. The absence of a residual market backstop means that if this experiment goes wrong, the fallout lands directly on policyholders, with no buffer, and the political and regulatory response would likely be swift and sweeping.

United Policyholders has already flagged this risk publicly, describing the law as a fundamental shift in how wildfire risk is allocated and raising specific concerns about notification gaps. Many policyholders will not know their standard policy no longer covers wildfire until they file a claim after a fire. That is not a hypothetical scenario. It is a claims outcome that, at scale, would generate significant adverse press, legislative backlash, and potentially new restrictions on the flexibility the law currently provides.

The sandbox framing is worth taking seriously. AB 376 is explicitly a four-year pilot. The regulatory permission it grants is not permanent. How carriers, MGAs, and the broader market behave during this window will determine whether the model survives or gets reversed.

Reinsurance and Treaty Implications

The unbundling of wildfire from a standard homeowners product creates real complexity on the reinsurance side, and this is an area where the industry has not yet developed consensus practices.

When wildfire is a component of an all-perils treaty, the aggregate exposure, the event definition, and the loss triggers are all structured around that bundled product. Separating wildfire into a standalone product means that exposure needs to be ceded under a different treaty structure, with wildfire-specific event definitions, zone-based aggregation, and potentially different attachment points than a traditional cat treaty would contemplate.

Reinsurers are not uniformly prepared for this. Some have been pushing for exactly this kind of perils separation for years, precisely because it allows for cleaner pricing and more accurate cat modeling. Others are uncertain how a standalone wildfire product at scale would perform, particularly in terms of adverse selection. The policyholders most likely to seek out and pay for a standalone wildfire policy are, by definition, those who perceive themselves to be at greatest risk. That is a meaningful underwriting consideration.

What Other States Are Likely to Do

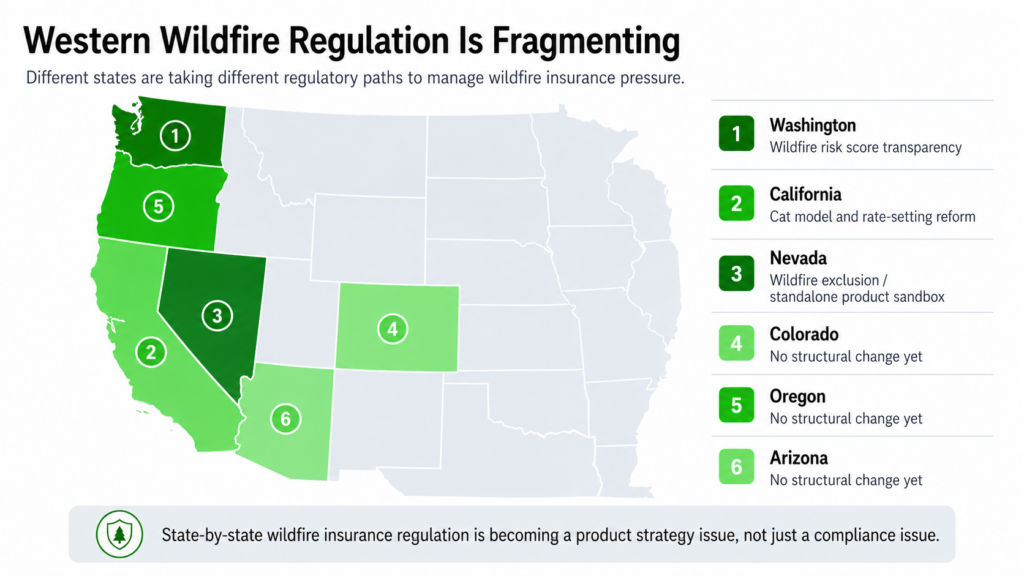

Nevada’s decision did not happen in isolation. It is part of a broader pattern of states experimenting with different approaches to managing the tension between wildfire risk pricing and insurance market availability. The approaches vary considerably.

California has maintained strict all-perils requirements in the admitted market while pursuing regulatory reform on rate-setting, moving toward a framework that allows carriers to use forward-looking catastrophe models rather than historical loss experience to price wildfire exposure. The tradeoff is that California still has multiple admitted carriers who have exited anyway, because even reformed rate approval processes have not moved fast enough to keep pace with actual risk costs.

Washington state recently passed a wildfire risk score transparency bill requiring carriers to disclose and explain the risk scores they use to make coverage and pricing decisions. This approach focuses on process transparency rather than product structure, and it creates a disclosure and appeals framework that could meaningfully affect underwriting operations for carriers active in the Washington market.

Colorado, Oregon, and Arizona are all managing significant wildfire exposure without having yet moved to the kind of structural product changes Nevada has permitted. Each is watching the Nevada experiment.

“State-by-state regulatory intelligence is no longer a compliance exercise. It is a product strategy input.”

The practical implication for carriers and MGAs with multi-state western books: the regulatory landscape for wildfire coverage is actively fragmenting. Assuming that what works in one state’s admitted market will translate cleanly to another is increasingly risky. State-by-state regulatory intelligence is no longer a compliance exercise. It is a product strategy input.

The Distribution and Communication Dimension

There is one aspect of AB 376 that the industry has underweighted in most of its analysis so far: the agent and policyholder communication challenge.

If carriers exercise the wildfire exclusion in Nevada, the burden of explaining the change falls primarily on the distribution chain. Agents and brokers will need to clearly communicate what is no longer covered, what the standalone wildfire product options are, and what policyholders need to do to maintain comprehensive coverage. This is not a simple conversation, particularly in a market where insurance literacy is already low and where policyholders have years of experience treating wildfire as an assumed component of their standard coverage.

Carriers that build robust agent education and clear policyholder notification processes into their approach to the Nevada exclusion will be in a fundamentally different position than carriers that treat the exclusion as a pure underwriting decision and leave the communication work to their distribution partners. The former approach builds distribution trust and reduces claim dispute exposure. The latter is a recipe for the kind of E&O exposure and reputational damage that tends to produce exactly the kind of legislative reaction that eliminates regulatory sandboxes.

The View from Property Guardian

Nevada’s AB 376 is genuinely significant market structure news, and the industry’s response to it over the next four years will shape how western states approach wildfire insurance regulation for the decade to come. The carriers, MGAs, and reinsurers who engage thoughtfully with what this experiment reveals will be better positioned than those who treat it as a Nevada-only story.

“As wildfire moves toward more granular, perils-based underwriting, the quality of the underlying property-level data becomes more important, not less.”

At Property Guardian, we work with carriers and MGAs to bring verified, property-level wildfire risk data into the underwriting and risk selection process. As the market moves toward more granular perils-based underwriting, the quality of that underlying data becomes more important, not less. Insureds with documented mitigation work are materially different risks than properties with no mitigation record, and in a world where wildfire is priced as a standalone peril, that difference needs to be quantifiable.

If you are thinking through how wildfire market structure changes affect your book, your treaty structure, or your product strategy in western states, we are glad to be a resource.

Sources

Nevada Current (Oct 2025) | National Mortgage News | United Policyholders | Nevada AB 376 legislative text