June 29, 2026

By Paul Brady, Head of Wildfire Insights & Mitigation

I recently attended Guy Carpenter’s 2026 California and Western States Summit in San Francisco, where leaders across wildfire risk, insurance, reinsurance, regulation, and resilience came together to discuss where the market is headed.

I also participated in the panel discussion, “The Evolution of Technology in Wildfire Risk,” alongside other technology companies focused on California wildfire tools and solutions.

The event made one thing very clear: the wildfire insurance market is making progress. The technology is improving. The science is becoming more practical. Regulators are more engaged. Carriers and reinsurers are asking better questions.

But the biggest takeaway was this:

The industry is moving beyond the wildfire risk score.

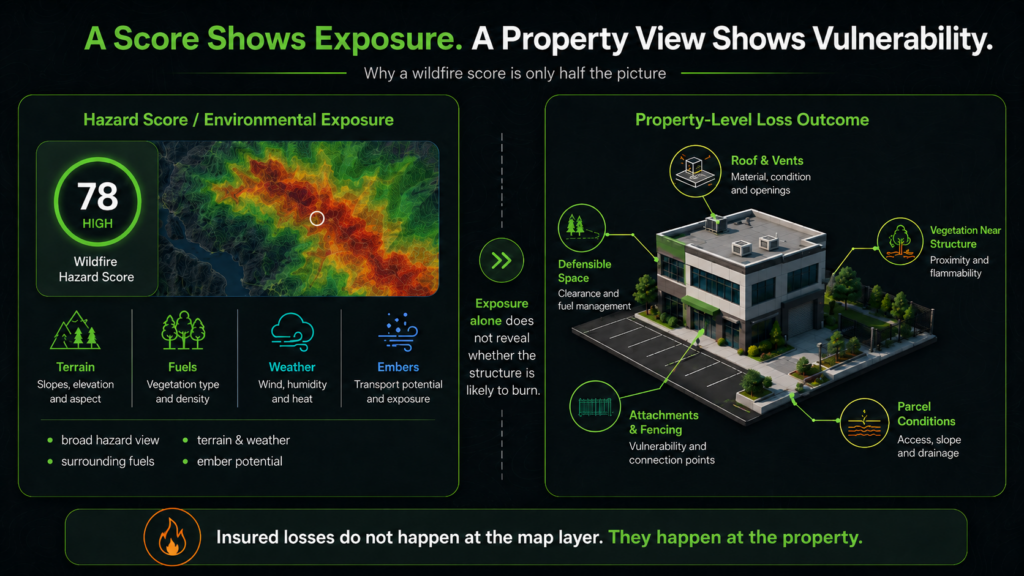

For years, wildfire underwriting has been dominated by broad hazard views. What is the score? What is the map layer? How close is the property to vegetation? Is the location inside or outside a high-risk zone?

Those questions still matter. But they are no longer enough.

The next era of wildfire underwriting will depend on a more complete view of risk, one that connects the environment, the structure, the parcel, the community, and the real-world conditions that determine whether a property can survive when fire arrives.

Here are five signs that shift is already underway.

1. Underwriters are realizing a wildfire score is only half the picture.

One of the most important conversations on our panel focused on what the insurance industry still gets wrong about wildfire risk.

A wildfire hazard score can tell you a lot about the environment around a property. It can help explain exposure to fuels, terrain, weather, ember potential, and historical fire behavior.

But it does not tell you whether the structure itself is likely to burn.

That distinction matters.

You can have a high-risk structure in a lower-risk environment. Embers may still land there. If the building has combustible materials, unmanaged vegetation, vulnerable vents, attached fencing, or poor defensible space, it may still be highly susceptible to ignition.

The reverse is also true. You can have a more defensible structure in a higher-risk environment because the property has been hardened, vegetation has been managed, and the immediate surroundings reduce ignition potential.

That is why the market has to move beyond asking, “What is the wildfire score?”

The better question is:

What is the relationship between the hazard, the structure, the parcel, and the likely loss outcome?

That is where underwriting is headed. The strongest approaches are beginning to separate environmental wildfire exposure from structure-level vulnerability. That shift is critical because insured losses do not happen at the map layer. They happen at the property.

2. Conflagration risk is now impossible to ignore.

Another major theme throughout the summit was conflagration risk, especially in denser communities where one burning structure can become the ignition source for the next.

For a long time, wildfire conversations focused heavily on vegetation-driven spread: fuels, slope, wind, ember cast, and fire moving across the landscape. Those factors still matter tremendously.

But recent fires have forced the industry to look harder at a different problem: structure-to-structure ignition.

In some communities, the risk is not only that wildfire reaches the neighborhood. It is that once a few structures ignite, the built environment itself becomes part of the fuel system.

That changes the underwriting conversation.

Parcel spacing matters. Building materials matter. Fences, decks, vents, and attachments matter. Neighboring structures matter. Community layout matters.

The exposure is no longer just “wildfire nearby.” It is whether the property can survive when embers, radiant heat, and nearby structural ignition begin interacting.

That is a much more complex risk problem. It is also one the market is beginning to take much more seriously.

3. Mitigation is becoming a shared language.

One of the most encouraging themes from the summit was the growing alignment around mitigation.

Insurance commissioners from multiple Western states spoke about the importance of mitigation standards and the need to connect insurance, government, homeowners, builders, and communities around practical risk reduction.

The Insurance Institute for Business & Home Safety (IBHS) came up repeatedly. That stood out.

What was once viewed largely as insurance-focused science is now showing up in broader conversations involving regulators, builders, public agencies, and community resilience leaders.

That is a meaningful shift.

It suggests the market is beginning to converge around a more consistent understanding of what “better” looks like. Not perfect. Not universal. But more aligned.

That matters because mitigation only works at scale when the market can recognize it.

Property owners need to understand which improvements actually reduce risk. Underwriters need to see whether those improvements are present. Regulators need confidence that mitigation is meaningful, measurable, and tied to real-world loss reduction. Carriers need a way to reflect better risk in appetite, pricing, or underwriting decisions.

We are not fully there yet. The industry still lacks standardization. Different carriers, regulators, communities, and property owners still operate with different assumptions and incentives.

But mitigation is becoming a common language. That is progress.

4. The insurance crisis is shifting from availability to affordability.

For several years, the wildfire insurance conversation has centered on availability.

Can homeowners and businesses get coverage at all? Will admitted carriers remain in the market? How much risk will flow into FAIR Plans or other residual markets?

Those concerns remain very real.

But the summit also highlighted a second challenge that is becoming harder to ignore: affordability.

Coverage may exist, but at a price many property owners struggle to absorb. That creates pressure across the entire system: homeowners, commercial property owners, agents, MGAs, carriers, reinsurers, regulators, and elected officials.

It also creates difficult tradeoffs.

“Coverage may exist, but at a price many property owners struggle to absorb.”

Some property owners may choose a FAIR Plan option or a less comprehensive coverage path because it appears faster, simpler, or cheaper, even if it may not provide the same level of protection.

That should concern the market.

If the private insurance market wants to pull risk back from residual markets, speed, clarity, confidence, and risk differentiation all matter. The industry has to identify which properties are truly poor risks, which are better than they appear, and which could become more insurable through targeted mitigation.

That cannot happen with broad-brush hazard screening alone.

It requires property-level intelligence.

5. Technology is advancing, but the system still needs to connect.

The summit made clear that wildfire technology is advancing quickly. There are better tools today for detection, monitoring, modeling, pricing, underwriting, mitigation analysis, and portfolio management than the industry had even a few years ago.

That progress is real.

But technology alone will not solve the wildfire insurance problem if the rest of the system remains disconnected.

A carrier can have better data, but if that data does not translate into underwriting action, the value is limited.

A regulator can support mitigation, but if carriers cannot consistently recognize mitigation in pricing or appetite, the impact is limited.

A property owner can invest in hardening and defensible space, but if those improvements are invisible to the market, the incentive breaks down.

That is the gap the industry has to close.

The next era of wildfire risk will not be defined by who has the most data. It will be defined by who can connect data to decisions.

At Property Guardian, that is where we believe the market has to go: beyond static scores, beyond generalized hazard views, and toward a more complete understanding of how each property is likely to perform when fire arrives.

That means understanding the surrounding environment. It means evaluating the structure. It means accounting for parcel conditions. It means recognizing community and suppression realities. And increasingly, it means understanding how nearby structures can influence one another in a conflagration scenario.

The Next Phase of Wildfire Underwriting

I left the summit encouraged, but clear-eyed.

The wildfire insurance market is not solved. Losses are increasing. Conflagration risk is better understood, but not fully quantified. FAIR Plan pressure remains a major concern. Affordability is becoming more difficult. And the industry still has work to do to align science, regulation, underwriting, and mitigation.

But the conversation has changed.

We are no longer debating whether wildfire risk requires better technology. We are debating how to apply that technology in ways that create a more stable, resilient, and insurable market.

That is progress.

The next step is connection.

Because the future of wildfire underwriting will not be built on a single risk score. It will be built on a connected view of risk, one that reflects the environment, the structure, the parcel, the community, and the real-world conditions that determine whether a property can survive.

That is the work ahead.

And it is the work Property Guardian is built to support.