June 25, 2026

By Brian Bastian, Head of Product

The commercial property market entered 2026 in a fractured state, and the fracture is no longer subtle. Across North America, wildfire coverage has split into what brokers are now openly calling a two-speed market. Urban, low-hazard locations are seeing rates stabilize. Properties in the wildland-urban interface remain elevated and tightly underwritten. And high-hazard assets face steep premium increases alongside a new condition of coverage: prove active mitigation, or face non-renewal. For commercial property underwriters, brokers, and corporate risk managers, the message is that a wildfire-exposed property is no longer a set-and-forget risk. It is an account that must continuously demonstrate why it deserves capacity.

“A wildfire-exposed property is no longer a set-and-forget risk. It is an account that must continuously demonstrate why it deserves capacity.”

Two recent developments sharpen the picture. New analysis from Gallagher Re shows that insured wildfire losses are no longer overwhelmingly concentrated in Southern California. Northern and Southern California now account for roughly equal shares of average annual industry loss, a rebalancing driven by warming conditions and decades of fuel buildup in the north. At the same time, carriers are moving risk evaluation down to the individual policy level, and that granularity is feeding directly into reinsurance pricing. The more precisely an insurer can demonstrate control over its accumulations, the more competitive its reinsurance financing becomes.

What the Two-Speed Market Actually Means

In practice, the market is sorting properties into lanes. Low-hazard urban risks sit in the fast lane, where competition and alternative capital have helped steady rates. Alternative capital, including catastrophe bonds and insurance-linked securities, reached roughly $121 billion in 2025, and a relatively quiet hurricane season left reinsurers with capacity to deploy. That capital flows readily to risks that are easy to model and easy to defend.

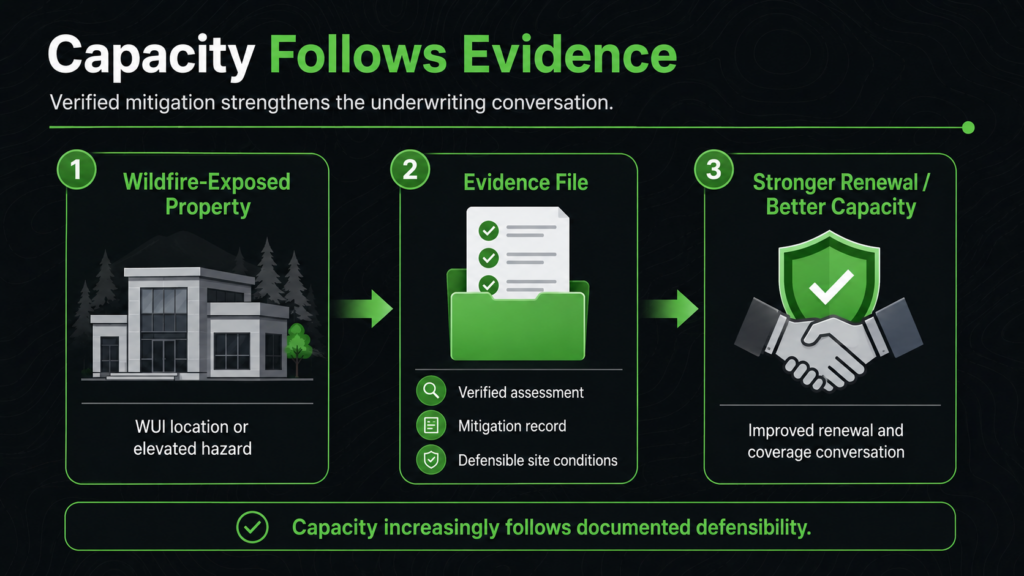

The slow lane is where wildfire-exposed commercial property lives. Here, many insurers now make coverage conditional on a professional wildfire assessment or a verified mitigation plan as part of underwriting. Documented mitigation has become the practical path to a better rate or to avoiding non-renewal at all. Premium credits for verified measures are real, but they are earned, not assumed. The properties that struggle are not always the ones with the worst construction. Often they are the ones that cannot produce evidence of what has been done and how defensible the site actually is.

Why Granularity Changes the Underwriting Conversation

For years, wildfire underwriting leaned on broad territory scores and hazard maps. That era is ending. As one market analysis put it, there is now intense focus on evaluating aggregation and financing costs at the policy level before a policy is ever written. Carriers that integrate modeling directly into their underwriting workflow are positioning to grow, but selectively. The ones that cannot are either retreating from wildfire-exposed segments or pricing so conservatively that they lose good business.

This is where the Gallagher Re finding lands hardest. If average annual loss is rebalancing toward Northern California, then portfolios built on the old assumption that the serious exposure sits in the south are carrying risk they have not priced. Granular, property-by-property evaluation is the only way to catch that drift before it becomes a loss surprise. The carriers winning capacity in 2026 are the ones who can show a reinsurer, account by account, exactly what they hold and why it is defensible.

The Variable Most Scores Still Miss

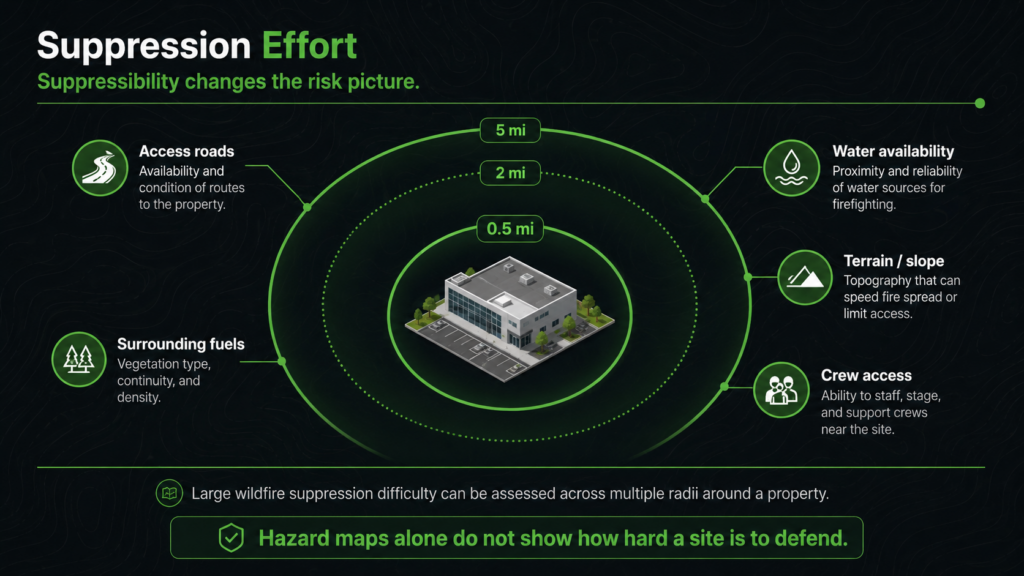

Even sophisticated catastrophe models tend to answer one question well: how likely is fire to reach this location and how much damage might it do. They are far weaker on a second question that determines outcomes on the ground. If a fire arrives, how realistically could it be suppressed here? Two properties with identical construction and identical hazard scores can have very different real-world fates depending on access, surrounding fuels, water availability, and the sheer difficulty of getting crews and equipment into position in time.

Traditional ISO and Protection Class scores do not capture this. They were built for structure fires in developed areas, not for a wind-driven wildfire bearing down on a commercial property in the interface. In a two-speed market that rewards precision, the suppressibility of a site is one of the most underpriced variables in the book, and one of the most decision-relevant when a carrier is choosing which lane an account belongs in.

Practical Takeaways for Commercial Property Teams

Build the evidence file before renewal, not during it. In a market where coverage is conditional on documented mitigation, the account that arrives with a verified assessment and a maintained mitigation record negotiates from strength. The account that arrives with assertions negotiates from weakness.

Re-underwrite Northern California exposure with fresh eyes. If your portfolio assumptions still treat the north as a lower-tier wildfire region, the Gallagher Re analysis is a prompt to revisit them at the policy level before the next event does it for you.

Separate hazard from defensibility on every WUI account. Ask not only how likely a fire is, but how hard it would be to stop one here. The second question is where the pricing edge increasingly lives.

Use granularity as leverage with reinsurers. The more precisely you can characterize each risk and your control over accumulations, the more competitive your treaty terms become. Policy-level rigor is no longer just good underwriting hygiene. It is a financing advantage.

Where Property Guardian Fits

A two-speed market rewards underwriters who can see what legacy scores miss, and the suppressibility of a site is at the top of that list. Property Guardian’s wildfire risk insight reports include a Suppression Effort measure that simulates large wildfires and quantifies how difficult it would be for boots on the ground to actively suppress a fire within the 0.5-mile, 2-mile, and 5-mile radii around a property. It is exactly the defensibility signal that hazard maps and ISO or Protection Class scores leave out. In a market where capacity follows precision, having that signal on every WUI account is what lets a team place a risk in the right lane with confidence, and show a reinsurer why.

Sources

Insurance Business, Behind the new wildfire risk reality for California property markets (Gallagher Re analysis).

SPIEDR, Wildfire Insurance Guide for Commercial Properties (two-speed market).

Amwins, State of the Market, 2026 Outlook.

Insurance Business, Commercial property insurance braces for a volatile 2026: