June 9, 2026

By Brian Bastian, Head of Product

There is a number attached to nearly every commercial building in Washington, and across most of the West, that quietly shapes whether it can be insured and what the premium will be. Most risk managers never see it, and few fully understand how it is produced. It is the property protection classification: a 1-to-10 grade for the fire-protection capability around a given location. On June 2, the Washington State Office of the Insurance Commissioner (OIC) published a report that said, in effect, that the way those scores are generated needs to change.

What the Report Actually Said

The OIC delivered its report to the state Legislature on May 28, after lawmakers requested a review of the Washington Survey & Rating Bureau (WSRB) and whether its rating methodology could be modernized. The WSRB is an independent bureau that collects data on fire departments, municipal water supplies, and emergency communications, then assigns each area a protection class from 1 (best protected) to 10. Insurance companies buy those scores and use them to decide whether to write a risk at all and how to price it.

To produce the report, consultants surveyed fire-service professionals across the state. Their single most pressing concern was a lack of transparency: it is difficult to understand how a classification is calculated, or how an investment of public funds (a new station, a tanker, an upgraded water main) would actually move a score. The report’s technical findings were just as pointed. The WSRB’s methodology, it concluded, does not reflect how fire departments perform during actual fire responses. Its fixed distance thresholds create ‘cliff’ effects, where minor geographic variations produce major classification swings. And rural and volunteer departments are evaluated against standards built for urban departments staffed full-time by career firefighters. The report recommends a structured pilot for performance-based fire-protection ratings.

Why an Obscure Rating Bureau Matters to Commercial Property Teams

The protection class is one of the quietest inputs in property underwriting, and one of the most consequential. It travels silently from the bureau into carrier rating engines, where it helps determine appetite, terms, and price. Because the score reflects community fire-protection capability rather than the characteristics of any single building, two commercial properties a few hundred feet apart can land on opposite sides of a ‘cliff’ threshold, and receive materially different premiums, deductibles, or coverage outcomes, despite being functionally identical risks.

“The protection class is one of the quietest inputs in property underwriting, and one of the most consequential.”

For a portfolio, an opaque or outdated methodology means mispriced risk in both directions. And when a bureau like the WSRB signals a shift toward performance-based metrics, that is advance notice that classifications, and therefore rates and capacity, could be re-drawn for entire categories of risk, especially in the rural and wildland-urban interface zones where commercial assets are increasingly exposed.

Washington is not acting in isolation. The report follows a wildfire-risk-scoring transparency bill that advanced through the state Senate earlier this year, and it echoes a broader regulatory current, including Colorado’s push to make insurer risk models more transparent, toward scoring that policyholders can see, understand, and contest. The direction of travel is clear: the era of treating a single proprietary score as unquestionable ground truth is ending, and the teams that benefit will be the ones who understand what sits underneath the number.

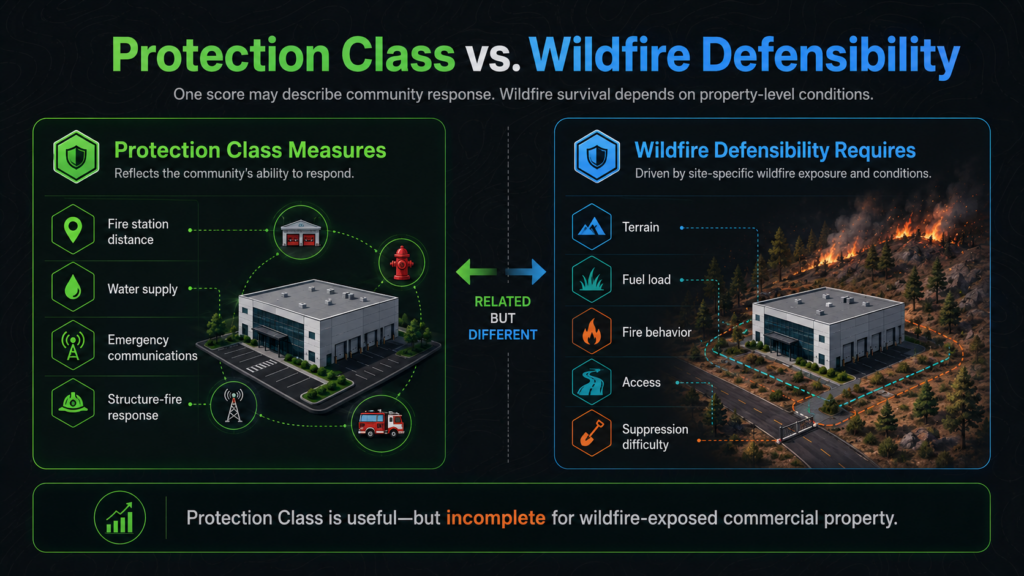

The Bigger Blind Spot: Protection Class Was Never Built for Wildfire

There is a more fundamental limitation the report only partly reaches. Protection classifications, like the ISO Public Protection Classification used elsewhere, were designed to predict outcomes for structure fires: a kitchen blaze, an electrical fault, an HVAC ignition. For that scenario the inputs make sense. How close is the nearest staffed station? How much water can the hydrant system deliver? How fast can an engine arrive? A well-protected community puts the fire out before it spreads, and the score captures that capability well.

A wind-driven wildfire breaks every one of those assumptions. Once a fire grows past 2,000 acres under extreme weather, it no longer matters how close the nearest station is, because the fire service is operating under a completely different doctrine. National wildland guidance is explicit about the priority order: human life first, then firefighter safety, and only then property. Defending structures ‘will not be possible in every situation.’ Crews build a containment strategy for the fire as a whole and triage which structures can be safely defended; in a major event, multiple fires across a region stretch personnel, engines, and aircraft past their limits. The engine that would have arrived in four minutes for a kitchen fire may be on a containment line miles away, or holding a road for evacuation.

In other words, the variable that actually governs whether a commercial property survives a large wildfire is not community fire-protection capability. It is suppression difficulty: whether terrain, fuel loads, fire behavior, and access would even allow crews to engage and hold ground near that specific property. The U.S. Forest Service has formalized exactly this concept in its Suppression Difficulty Index, which combines topography, fuels, expected fire behavior under severe weather, firefighter line-production rates, and accessibility to estimate how hard a fire would be to suppress in a given location. None of that is captured in a Protection Class score, and yet it is decisive in precisely the events that produce catastrophic commercial losses.

Practical Takeaways for Commercial Property Teams

For underwriters and risk managers:

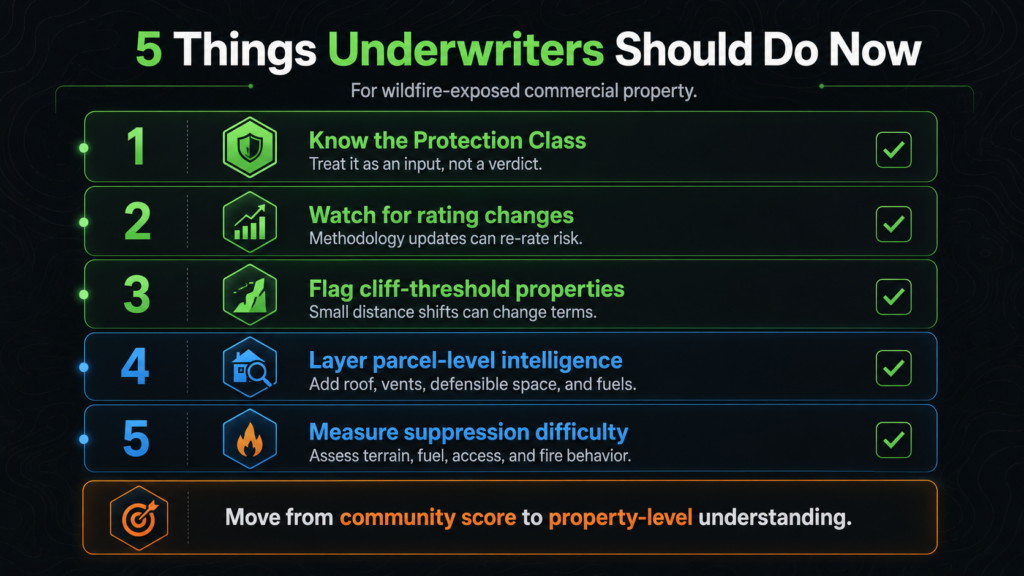

- Know the protection class for every location in your book, and, where you can, the basis for it. Treat it as an input to interrogate, not a verdict to accept.

- Do not assume the score is static. Methodology modernization in Washington (and likely other states) could re-rate properties up or down, with direct consequences for pricing and capacity.

- Flag properties sitting near ‘cliff’ thresholds. A small change in distance methodology can swing a classification, so identify where that exposure concentrates in your portfolio before the bureau does.

- Layer parcel-level intelligence on top of the community score. A protection class measures the neighborhood’s structure-fire capability; it says nothing about a specific building’s roof, vents, construction materials, defensible space, or proximity to fuel.

- For wildfire-exposed risks, weigh suppression difficulty separately. In a large wind-driven fire, station proximity stops mattering. What matters is whether terrain, fuel, and access would let crews engage near the property at all. A strong Protection Class does not mean a property is defensible in a conflagration.

For operators of insured commercial properties:

- Document your site-level mitigation independently. Verified hardening and defensible space give you something concrete to bring to renewal conversations, and a basis to question a score that does not reflect reality on the ground.

- Engage early with local fire-service investments. The report makes clear that the link between public investment and score improvement is poorly understood; getting ahead of it can protect both safety and insurability.

None of this replaces the bureau score. It contextualizes it. When the community grade is in flux, and Washington has just signaled that it is, the underwriters and risk managers who can speak to the actual condition of the actual building will be the ones making confident decisions while others wait for the methodology to settle.

How Property Guardian Helps

This is the gap Property Guardian is built to close. A Protection Class tells you how well a community can stop a structure fire. It does not tell you whether anyone could realistically defend your insured property when a 2,000-acre fire is running toward it, and that is the scenario that drives catastrophic loss. Our wildfire risk insight reports address this directly with a dedicated Suppression Effort measure. By simulating large wildfires around the property, we quantify how difficult it would be for boots on the ground to actively suppress a fire within the 0.5-mile, 2-mile, and 5-mile radii surrounding it, turning terrain, fuel, and access into a concrete, parcel-level signal.

“The variable a community score leaves out is not just how the property might burn, but how hard it would be to save.”

Paired with our assessment of the building’s own construction and vulnerability, that gives underwriting and risk teams the variable a community score leaves out: not just how the property might burn, but how hard it would be to save. When bureau ratings are being rewritten, that ground-truth picture lets your team price, defend, and manage wildfire exposure on the merits of the property itself, not on a grade designed for a different kind of fire.

Sources

Insurance Journal, “Report Calls for Transparency, Modernization of Washington Fire Scoring Bureau” (June 2, 2026): https://www.insurancejournal.com/news/west/2026/06/02/872044.htm

Insurance Journal, “Wildfire Risk Scoring Transparency Bill Passes Washington Senate” (Feb. 13, 2026): https://www.insurancejournal.com/news/west/2026/02/13/857963.htm

NWCG, Wildland Urban Interface: Structure Protection (firefighting priorities): https://www.nwcg.gov/6mfs/operational-engagement/wildland-urban-interface-structure-protection

Firehouse, “How Firefighters Determine Control Objectives of a Wildfire” (the containment box): https://www.firehouse.com/operations-training/wildland/article/53061809/how-firefighters-determine-control-objectives-of-a-wildfire

U.S. Forest Service Research & Development, Suppression Difficulty Index: https://research.fs.usda.gov/rmrs/products/dataandtools/suppression-difficulty-index

Colorado General Assembly, HB25-1182, Risk Model Use in Property Insurance Policies: https://leg.colorado.gov/bills/hb25-1182