June 2, 2026

By Brian Bastian, Head of Product

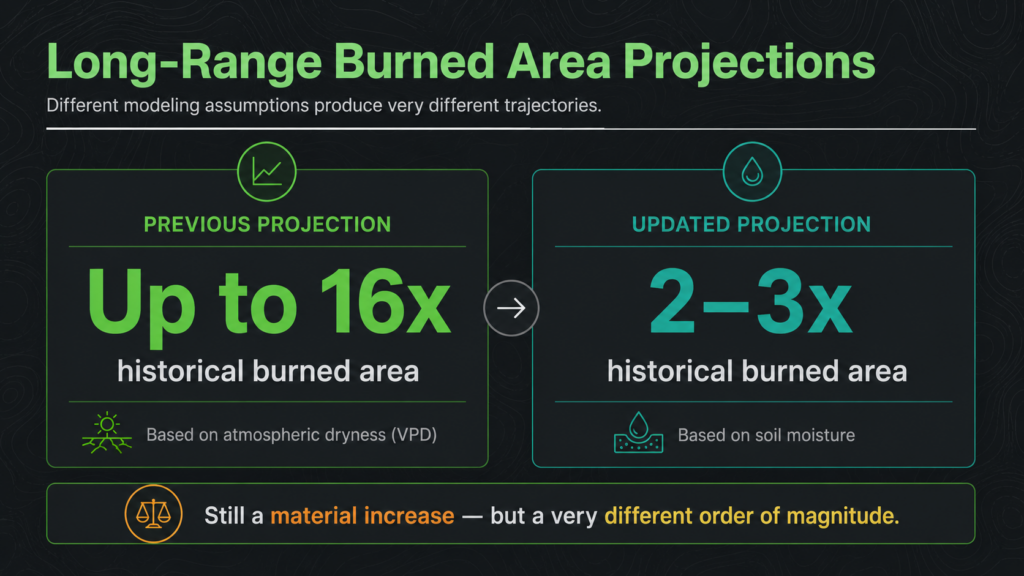

For more than a decade, the wildfire risk conversation in the insurance industry has been shaped by a set of alarming long-range projections: under continued warming, the area burned by wildfires in the Western United States could grow dramatically. Some climate models have suggested increases of 10 to 16 times historical levels by the time global temperatures rise 3 degrees Celsius.

Those projections have influenced reinsurance pricing, multi-year carrier strategy, and the climate change loadings that some modelers apply on top of historical CAT baselines. They are part of the backdrop against which the industry has been making long-horizon decisions about wildfire-exposed portfolios in California, Colorado, and across the Western WUI.

New research published in April 2026 in AGU Advances, a peer-reviewed journal of the American Geophysical Union, argues that those long-range projections may have been overestimated by as much as an order of magnitude. The implications are not about the CAT model outputs your underwriters run today; they are about the long-term risk trajectory assumptions embedded in reinsurance pricing, climate-adjusted portfolio strategy, and the science underlying future model updates. Here is what the research says and why it matters.

The Science: Why Previous Projections May Have Overshot

The study challenges a core assumption that has underpinned most long-range wildfire projection models: that atmospheric dryness, specifically vapor pressure deficit (VPD), is the primary driver of how much area will burn under future climate conditions.

VPD is relatively easy to measure and project under climate scenarios, which is why it became the standard proxy for wildfire fuel dryness in long-range modeling. The problem, the researchers argue, is that it is the wrong proxy. Atmospheric dryness is not the same as fuel dryness. The moisture content of the vegetation and soil that actually burns is better captured by soil moisture, a measure that responds to precipitation patterns, vegetation water uptake, and land surface hydrology rather than atmospheric conditions alone.

When the researchers used soil moisture rather than VPD to model how fuel dryness changes under warming scenarios, the projected increase in burned area dropped dramatically. At 3 degrees Celsius of warming, VPD-based models projected burned area increases of up to 16 times the historical baseline. Soil-moisture-based models suggest the actual increase may be only 2 to 3 times. That is still a material increase over the coming decades, but a fundamentally different order of magnitude.

The team analyzed five forested ecoregions in the western states using the Western U.S. MTBS-Interagency wildfire dataset from 1984 to 2020, giving the analysis a robust empirical foundation.

What This Study Does and Does Not Address

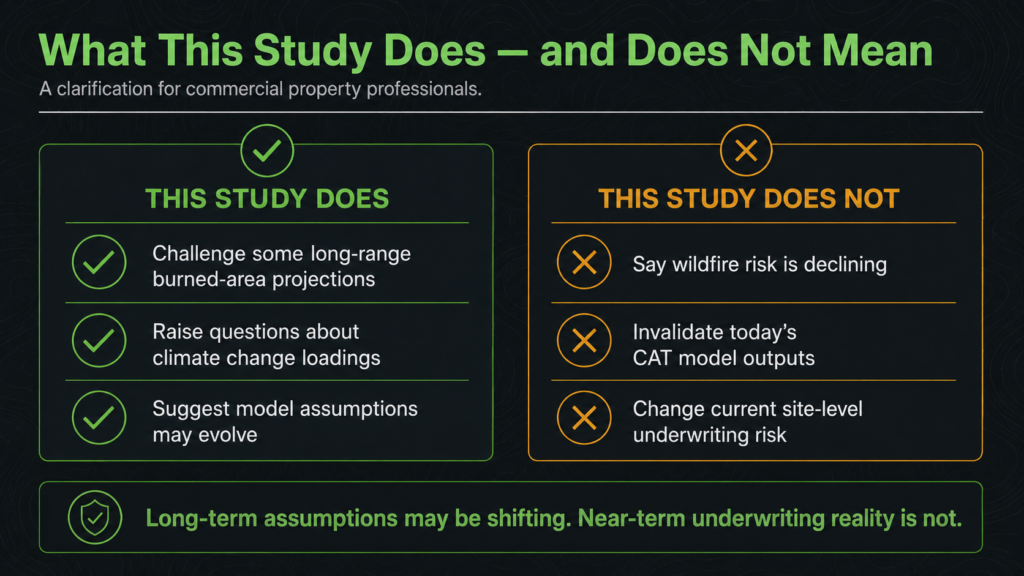

Before drawing implications for commercial property underwriting, it is worth being precise about what this research actually covers.

It is a long-range climate projection study, not a CAT model validation. The commercial catastrophe models your underwriting teams use today (from vendors such as Moody’s RMS, Verisk AIR, and CoreLogic) are primarily calibrated to historical fire data and current hazard conditions: vegetation, topography, fuel loads, and weather patterns. They generate stochastic event sets based on what has happened in the past. The AAL figure from a standard CAT run reflects current-conditions hazard, not a multi-decade climate trajectory. This study does not directly challenge those near-term outputs.

What the study does challenge is the science underlying climate change loadings. Some modelers and reinsurers apply adjustment factors on top of historical CAT baselines to account for future warming, and those adjustments may draw on exactly the kind of VPD-based projections the AGU research questions. It also speaks directly to the long-horizon thinking that shapes reinsurance pricing, carrier appetite strategy, and portfolio-level wildfire exposure decisions over multi-year timeframes.

The research also does not say wildfire risk is declining. Observed data confirms that extreme wildfires have become more frequent, more intense, and larger over the past two decades, with the largest increases in Western U.S. temperate conifer forests. The January 2025 Los Angeles fires caused over $22 billion in insured losses in a real climate with real properties. What the research challenges is the trajectory of burned area growth at extreme warming levels over the long term, not current conditions.

Where the Implications Are Real for the Industry

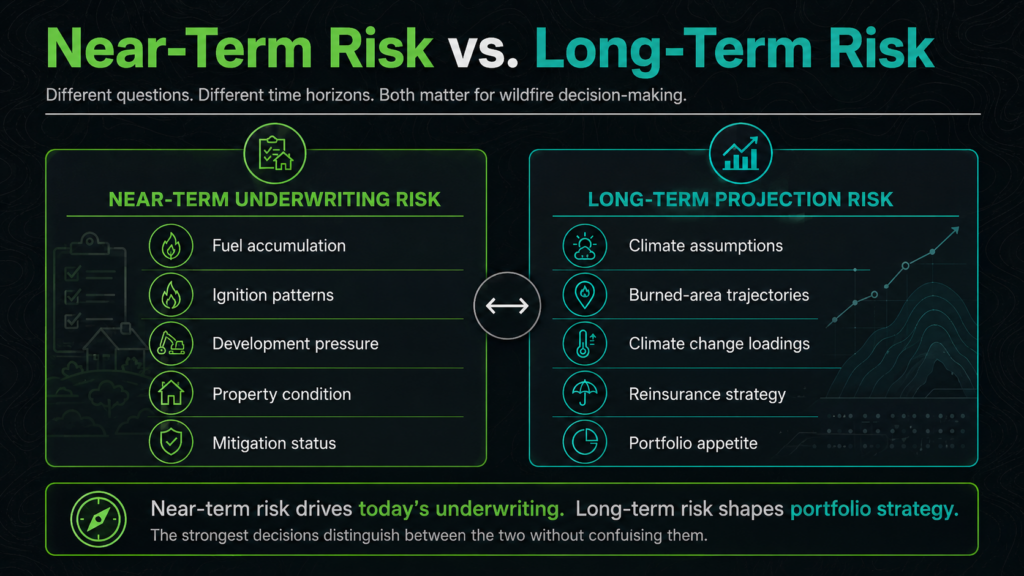

For day-to-day commercial property underwriting, this study is background context rather than an immediate action item. The near-term hazard profile of a WUI-exposed property does not change because a climate projection model has been revised.

But for several segments of the industry, the implications are more direct:

- Reinsurers and ILS investors pricing multi-year wildfire exposure who rely on climate-adjusted loss projections should be asking whether the adjustment factors they are using reflect current science or are built on VPD-based assumptions that this research challenges.

- CAT model vendors who have incorporated climate change loadings into their products will need to evaluate whether updated projection methodology affects those loadings. Model updates take time, but underwriters should be aware that changes may be coming.

- Carriers and MGAs conducting long-range portfolio strategy reviews, including decisions about market exits or appetite restrictions in WUI zones, are often implicitly relying on some version of the long-range burned area projections this research revises.

- Risk managers responsible for multi-year property programs should understand that the scientific basis for long-horizon wildfire risk is actively evolving and that some of the most alarming projections driving carrier behavior may be subject to downward revision.

“The near-term hazard profile of a WUI-exposed property does not change because a climate projection model has been revised.”

What Has Not Changed: Site-Level Risk Remains Real

The AGU study addresses landscape-scale burned area projections. It does not change the fundamental reality that individual commercial property outcomes in a wildfire are driven by site-level factors: construction materials, roof design, venting, defensible space, ember resistance, and proximity to fuel loads.

The California Department of Insurance and NAIC study published in March 2026 reinforced this point clearly. Rebuilding the communities destroyed in the January 2025 Los Angeles fires to the IBHS Wildfire Prepared Home standard would reduce Average Annual Loss by one-third, modeled using Moody’s wildfire catastrophe model. That reduction came from hardening individual structures and managing the immediate vegetation zone, not from any change in the landscape-level fire environment.

For commercial property risk managers, the takeaway is consistent with the science: the most actionable risk reduction lever available today is site-level mitigation. This remains true regardless of how long-range burned area projections evolve.

Practical Takeaways for Commercial Property Underwriters and Risk Managers

- Distinguish near-term from long-term risk drivers. The near-term wildfire hazard profile of WUI-exposed properties is driven by fuel accumulation, ignition patterns, and development pressure. That profile has not changed. Revised long-term burned area projections do not diminish the near-term underwriting challenge.

- If your organization applies climate change loadings to CAT model outputs, ask where those loadings come from and whether the underlying projection methodology is VPD-based or soil-moisture-based. This is a legitimate technical question to bring to your modeling vendor.

- For reinsurance program design and multi-year portfolio strategy, be aware that the scientific basis for long-horizon wildfire loss projections is actively being revised. Building too much conservatism into long-term strategy based on projections that may prove overstated carries its own risk.

- Site-level mitigation remains the most reliable and immediate risk reduction tool. Whether long-range projections settle at 2x or 16x the historical baseline, properties with documented structural hardening, ember resistance, and defensible space have better outcomes in actual fire events and better underwriting outcomes in the current market.

- Monitor regulatory developments. Washington’s wildfire risk score transparency legislation, passed by the state Senate in early 2026, signals that regulators are scrutinizing how risk scores are calculated and communicated. Revisions to the underlying science will eventually flow through to risk scoring methodologies and what regulators expect carriers to disclose.

The Bottom Line

New science does not make wildfire risk go away. It adds important nuance to how we project it over long time horizons and raises legitimate questions about the climate adjustment assumptions baked into some long-range pricing and strategy decisions.

For commercial property underwriters focused on near-term book management, the immediate takeaway is modest: be aware that long-range projection science is shifting and that model updates may follow. For reinsurers, ILS investors, and carriers making multi-year appetite decisions, the questions are more pressing and worth raising with modeling partners now.

“New science does not make wildfire risk go away. It adds important nuance to how we project it over long time horizons.”

Wildfire is one of the most dynamic perils in commercial property insurance. The science underpinning long-range risk projections is being actively revised by researchers, and modelers will follow. The organizations best positioned to navigate this environment are those that understand both the current near-term hazard and the evolving long-term picture clearly enough to distinguish between the two.

Property Guardian works with commercial property underwriting teams and risk managers to build assessment frameworks grounded in current science and current site conditions. Contact us to discuss how we can support your wildfire risk program.

Sources

AGU Advances: Large Overestimation of Projected Western U.S. Wildfire Burned Forest Area With Warming

AGU Newsroom: Future wildfires may burn less of the American West than expected (April 23, 2026)

Phys.org: How much worse could western wildfires get? New modeling changes projections (May 2026)

California DOI: Landmark study shows rebuilding Los Angeles to wildfire safety standards could slash future fire losses

Insurance Journal: Study: Rebuilding LA to Wildfire Safety Standards Could Lower Future Fire Losses