March 24, 2026

By Brian Bastian, Head of Product

Insurance regulators have been paying close attention to third-party wildfire risk scores for two years. Washington has now taken one of the clearest steps yet — and carriers who view this as only a Pacific Northwest issue may be underestimating what comes next.

The Washington State Senate passed Senate Bill 5928 — the Wildfire Risk Scoring Transparency Act — by a 48-1 vote. The bill, championed by Insurance Commissioner Patty Kuderer and now moving through the House, requires carriers to disclose the third-party wildfire risk scores used in underwriting decisions, explain the factor-level inputs driving those scores in plain language, provide policyholders with specific mitigation steps that would improve their score, and establish a formal appeals pathway when policyholders contend that completed mitigation work has not been reflected in their current score.

“Washington has now taken one of the clearest steps yet — and carriers who view this as only a Pacific Northwest issue may be underestimating what comes next.“

We have an obvious stake in how this legislation develops — Property Guardian is itself a wildfire risk scoring vendor of sorts. But that vantage point is exactly why we think this legislation is worth taking seriously rather than defensively. The carriers and vendors who engage with SB 5928 as a compliance problem to minimize are going to find themselves on the wrong side of a regulatory trend that has significant bipartisan momentum and a compelling consumer narrative behind it. Those who engage with it as a product design challenge – how do we build scores that are transparent, mitigation-responsive, and defensible – will be better positioned in every market where this comes next.

The Operational Compliance Problem for Carriers

Start with the most immediate challenge: workflow. Most carriers using third-party wildfire scores are receiving a score output — not a transparent, factor-weighted model they can freely disclose. The underlying methodologies are often proprietary. Factor weighting may be trade-secret protected. Data refresh cadence varies widely.

SB 5928 does not require carriers to expose vendor methodology in full. But it does require them to communicate, in plain language, what factors drove the score assigned to a specific property — and to do so in the context of an adverse underwriting action. That creates an immediate question many carriers haven’t had to answer operationally: what is your chain of custody from a third-party score output to a compliant, factor-level consumer disclosure?

Carriers who have built integrations with vendors that provide factor-level attribution will be in a stronger compliance position. Those relying on summary score outputs with limited factor transparency face a disclosure gap they will need to close — either by renegotiating data agreements or by building a translation layer between the score and the required disclosure language. Either path takes time, and the compliance clock is running.

“What is your chain of custody from a third-party score output to a compliant, factor-level consumer disclosure?”

This is also, notably, a vendor selection issue. Not all scoring providers are architected the same way with respect to factor transparency. Carriers reviewing their vendor relationships in anticipation of SB 5928 — or its inevitable successors in California, Colorado, and Oregon — should be asking scoring vendors directly: can you provide factor-level attribution at the individual property level, in a format that supports consumer-facing disclosure? The answer will tell you a great deal about the vendor’s regulatory readiness.

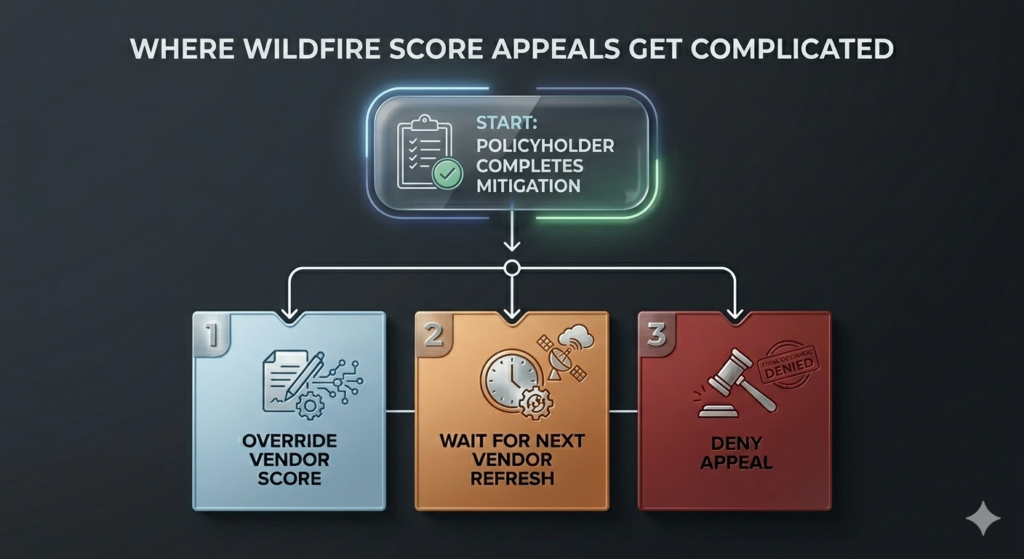

The Appeals Mechanism: Where It Gets Complicated

The appeals provision is the piece of SB 5928 that deserves the most careful attention from underwriting teams. The bill creates a formal process by which a policyholder can challenge a wildfire risk score — specifically in cases where mitigation work has been completed since the property was last evaluated and the carrier’s score does not reflect that work.

This introduces a dynamic the industry has largely avoided until now: the underwriting score as a living, contestable document rather than a static data input.

Consider what this means in practice. A policyholder completes IBHS Wildfire Prepared Home certification — new Class A roofing, ember-resistant vents, Zone 0 hardening, defensible space clearance. They submit documentation. Under SB 5928, the carrier must have a process to evaluate that documentation, determine whether the score should be updated, and respond within a defined timeframe.

This creates real underwriting tension. If a carrier is using a score from a vendor who refreshes property-level data annually — or less — the score may be structurally incapable of reflecting recent mitigation, regardless of what the policyholder has done. The carrier then faces three uncomfortable options: (a) override the vendor score based on submitted documentation, effectively running a parallel underwriting process; (b) defer the appeal pending the next vendor data refresh, which may not satisfy the bill’s timeline requirements; or (c) deny the appeal with an explanation that will not satisfy the policyholder or the regulator.

From our perspective as a scoring vendor, we think this is the right problem for the industry to be wrestling with. A score that cannot reflect real-world property improvements is a score that will increasingly face regulatory and legal challenge — in Washington first, and then everywhere else. The appeals mechanism in SB 5928 is uncomfortable for vendors whose architectures weren’t built for mitigation-responsiveness. It is much less uncomfortable for those whose were.

The Proprietary Score Tension

There is a subtler risk embedded in the factor disclosure requirement that the vendor community needs to think through carefully: the gradual erosion of methodological opacity as competitive moat.

If carriers are required to disclose, at scale, the specific factor-level outputs driving scores for individual properties, the aggregate of those disclosures creates a dataset from which sophisticated observers can begin to reverse-engineer model weights. This is not theoretical — it is the same dynamic that played out in credit scoring after ECOA adverse action notice requirements were established. The factor disclosure requirements that followed didn’t expose the FICO algorithm directly, but they created enough transparency that the industry adapted around it.

For vendors whose primary competitive advantage is methodological opacity, this is a genuine concern. For vendors whose advantage lies in data quality, model accuracy, and the ability to reflect property-level conditions in near-real time — transparency requirements are less threatening. The question every carrier should be asking their scoring vendors is: which of those descriptions fits you?

Carriers should also be reviewing their vendor contracts now to confirm they have the rights to make the factor-level disclosures SB 5928 will require. Some vendor licensing agreements restrict how score outputs can be shared. That is a contractual problem that needs to be identified before it becomes a compliance problem.

Adverse Selection: A Real Risk with a Defensible Answer

Critics of mandatory score disclosure have raised a concern worth taking seriously: if scores become effectively public information, it creates adverse selection dynamics that could undermine actuarial integrity. The argument is that policyholders who receive good scores will use that information to aggressively shop for lower premiums, while those with poor scores will invest in mitigation, appeal, and then shop once their score improves — leaving the original carrier holding the cost of the disclosure and appeals process while the improved-risk benefit accrues to a competitor.

This is a legitimate structural concern. But it has a countervailing argument that we find more persuasive: if mitigation guidance actually works — and the IBHS loss research is increasingly clear that structure and parcel-level interventions materially affect both ignition probability and loss severity — then aggregate risk in the portfolio genuinely decreases when policyholders act on it. The adverse selection risk is real but manageable if carriers build retention incentives for improved-risk policyholders. The carrier who can say “we helped you improve your score, and here’s the premium recognition for it” has a much stronger retention story than the carrier who issued the non-renewal.

What Washington Means for California, Colorado, and Beyond

Washington is not the largest wildfire insurance market in the country, and SB 5928 will not reshape the national landscape on its own. But it matters for a specific reason: it provides a tested legislative template at precisely the moment when regulators in larger markets are actively looking for one.

California’s Department of Insurance has been pushing for greater transparency in carrier underwriting models as part of its sustainable insurance strategy. The FAIR Plan examination released in February 2026 — which found systemic failures in claims handling and consumer communication across 17 critical regulatory areas — has intensified pressure on the commissioner to demonstrate that market reform extends beyond rate approval mechanics to the underlying risk assessment infrastructure. Score disclosure legislation modeled on SB 5928 is a logical next step, and California’s market size means the compliance implications would be orders of magnitude larger.

Colorado’s Division of Insurance has been scrutinizing carrier non-renewal practices and the role of risk scoring in those decisions. Oregon and Arizona have active insurance reform working groups. The 48-1 vote in Washington’s Senate is not a regional quirk — it is a bipartisan signal that this issue has crossed the threshold from regulatory concern to political consensus.Carriers operating multi-state books in the wildfire corridor should be treating SB 5928 as an advance compliance exercise, not a Washington-specific obligation.

“Property Guardian’s wildfire risk scores are built around factor-level transparency, mitigation-responsiveness, and documentation integration”

What This Means for How We Build Scores

Speaking as a scoring data provider: SB 5928 is not a surprise to us, and it is not a threat to our product architecture. Property Guardian’s wildfire risk scores are built around factor-level transparency, mitigation-responsiveness, and documentation integration — because we designed them for a regulatory environment that we believed was coming. The bill’s requirements for factor disclosure, plain-language mitigation guidance, and an appeals process are things our platform supports as core features, not compliance patches.

For carriers evaluating scoring vendors in anticipation of expanded disclosure requirements, the differentiating questions are straightforward: Can the vendor provide factor-level attribution at the property level? How frequently is property-level data refreshed? Does the platform support documentation intake for mitigation appeals? Can the vendor produce consumer-facing disclosure language that meets a plain-language standard?

If a vendor can’t answer all four of those questions affirmatively, the SB 5928 compliance burden will land disproportionately on the carrier — not the vendor.

Property Guardian offers wildfire risk scoring built for the transparency era — factor-level attribution, near-real-time property data, integrated mitigation documentation, and consumer-facing disclosure support. If you’re a carrier evaluating your scoring infrastructure in anticipation of expanded regulatory requirements, we’d welcome the conversation.

Sources

Insurance Journal (February 13, 2026): Wildfire Risk Scoring Transparency Bill Passes Washington Senate

Insurance Business Magazine: Washington Senate bills would implement public wildfire risk scores and obstruct nonrenewals

California Department of Insurance (February 2026): Commissioner Lara and Assemblymember Calderon announce Make It FAIR Act

Washington Office of the Insurance Commissioner: 2026 Legislative Priorities