April 1, 2026

By Brian Bastian, Head of Product

Here is a fact that will surprise most homeowners: as of early 2026, there are no enforceable national standards for how smoke-damaged homes should be tested, cleaned, or restored after a wildfire. None. Not in California, not in Oregon, not anywhere in the United States.

That legal vacuum has had real consequences. Following the catastrophic Palisades and Eaton fires in January 2025, more than 42,000 insurance claims were filed. Among those, more than 13,000 involved standing homes — homes that did not burn, but were contaminated by wildfire smoke. For thousands of families, what followed was not a clear claims process. It was a prolonged argument over what “smoke damage” even means, who gets to test for it, what levels of contamination require remediation, and what “restored to pre-loss condition” actually looks like.

In the absence of standards, insurers and policyholders were essentially making it up — and predictably, they disagreed. Families sat in hotel rooms. Children were kept out of their homes over fears of toxic ash residue. Claims dragged on for months.California’s response is AB 1795, the Smoke Damage Recovery Act — legislation advancing through the state legislature right now that would establish the nation’s first enforceable standards for smoke damage claims.

What Is Smoke Damage, Really?

Before we can understand why this legislation matters, it helps to understand what smoke damage actually does to a home.

Wildfire smoke is not just a smell. It is a complex chemical mixture containing fine particulate matter, volatile organic compounds, heavy metals, and toxins from burned materials — including household chemicals, treated lumber, plastics, and in older neighborhoods, asbestos and lead paint. When smoke infiltrates a home, it doesn’t just coat surfaces. It penetrates HVAC systems, insulation, wall cavities, and porous materials like drywall and wood.

A home that appears structurally sound after a nearby wildfire may have contamination levels that pose genuine health risks, particularly for children, elderly residents, and people with respiratory conditions. But without testing standards, determining how contaminated a home is — and how thoroughly it must be cleaned — is a subjective call that creates enormous opportunity for disputes.

Insurance companies, understandably motivated by cost, may argue that surface cleaning is sufficient. Homeowners, fearing for their families’ health, may demand full remediation. Without objective standards specifying what tests to run, what contamination thresholds trigger what level of response, and what ‘restored’ means, both sides end up in a prolonged legal and financial limbo.

“California’s response is AB 1795, the Smoke Damage Recovery Act — legislation… that would establish the nation’s first enforceable standards for smoke damage claims.”

What AB 1795 Would Do

The Smoke Damage Recovery Act, introduced by Insurance Commissioner Ricardo Lara and Assemblymember Mike Gipson, would create a framework to end that limbo. The bill’s key provisions include:

- Statewide inspection, sampling, and testing protocols: For the first time, there would be consistent standards for how smoke-damaged homes are evaluated — what tests are performed, by whom, and what the results mean.

- Consistent remediation requirements: Insurers would be required to follow specific standards for restoring homes to their pre-loss condition. ‘Clean enough’ would have a legal definition.

- A 30-day inspection timeline: After a claim is filed, insurers would be required to inspect smoke-damage claims within 30 days and meet defined timelines for claim payments. This directly addresses one of the most common complaints from LA fire survivors: months of delays while families couldn’t return home.

- Protections for additional living expenses (ALE): Under AB 1795, insurers could not terminate ALE benefits — the payments that cover temporary housing — until a home has been tested and cleared as safe for habitation. This closes a significant loophole where insurers could end ALE payments before a home was actually habitable.

- An early action provision: Recognizing that the legislative process takes time, AB 1795 includes a mechanism that allows current wildfire survivors in Los Angeles to use any local or state health standards for smoke testing and remediation immediately, rather than waiting for the bill to become law. This is a meaningful step toward getting families into or out of their homes with clarity.

The bill is expected to be heard in an Assembly policy committee next month.

Why This Matters Beyond California

California often sets the policy template for the rest of the country on environmental and consumer protection issues. What happens with AB 1795 will be watched closely by state legislators in Oregon, Washington, Colorado, and Texas — states that face growing wildfire exposure but have no smoke damage standards of their own.

There is also a broader insurance market implication. Clear remediation standards benefit everyone in the claims ecosystem. Public adjusters, contractors, and restoration firms will have consistent guidance. Insurers will be able to price smoke damage risk more accurately once there is a defined scope of what remediation entails. And homeowners will have a legal framework to stand on rather than a negotiation they are almost always going to lose.

The federal dimension is also relevant. Two bills — the Wildfire Insurance Coverage Study Act of 2025, introduced in both the House (H.R. 550) and Senate (S. 2430) — call for a comprehensive federal study of wildfire insurance coverage gaps. If enacted, these bills could eventually produce national-level standards that don’t require every state to legislate separately.

What Homeowners Should Do Right Now

Whether or not AB 1795 becomes law, this moment highlights a set of actions every homeowner in a wildfire-prone area should take before fire season arrives:

- Review your policy’s smoke damage language today. Many standard homeowner policies cover ‘direct physical loss’ — but insurers often dispute whether smoke contamination qualifies. Ask your agent specifically how your policy handles smoke damage claims.

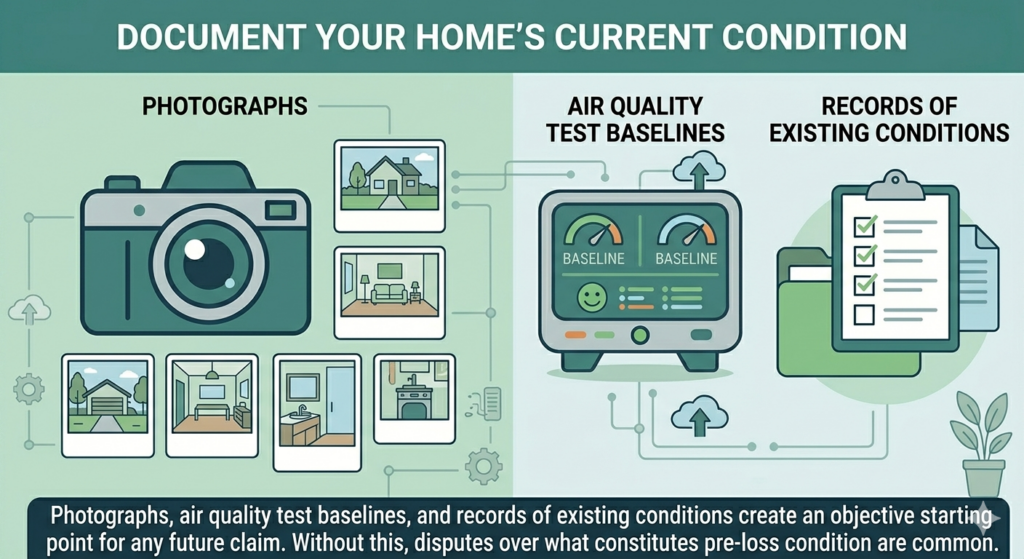

- Document your home’s current condition. Photographs, air quality test baselines, and records of existing conditions create an objective starting point for any future claim. Without this, disputes over what constitutes pre-loss condition are common.

- Track the bill’s progress. If you’re near the LA fire areas and have a pending claim, the early action provision of AB 1795 — once enacted — may give you immediate tools to push your insurer to follow consistent standards.

- Understand what your ALE coverage actually covers. Know the dollar limits and time limits on your additional living expenses coverage. If a smoke event forces you from your home, how long can your policy support temporary housing?

- Ask about home hardening’s connection to smoke mitigation. Many of the same measures that reduce a home’s ember ignition risk — sealed eaves, tight-fitting vents, weatherstripping — also reduce smoke infiltration. Two problems, one set of solutions.

A Final Thought

The Palisades and Eaton fires made a devastating point about smoke damage in the starkest possible terms: tens of thousands of families whose homes did not burn are still dealing with health concerns, insurance disputes, and uncertain timelines more than a year later. They did not lose their homes to fire. But in many cases, they effectively lost their ability to live in them.

“They did not lose their homes to fire. But in many cases, they effectively lost their ability to live in them.”

California’s Smoke Damage Recovery Act is a direct response to that reality. It is long overdue — and if enacted, it will set a national precedent for how we think about the full scope of wildfire damage, not just the dramatic images of burned structures.At Green Shield Risk, our Property Guardian approach is built on comprehensive risk awareness — including the often-underestimated risk of smoke damage. If you’d like to understand how your property and your insurance policy are positioned before fire season arrives, we’re here to help you think it through.

Sources

California Department of Insurance: Commissioner Lara and Assemblymember Gipson Unveil the Smoke Damage Recovery Act

Claims Journal: Nation’s First Smoke Damage Standards Bill Making Its Way Through California Legislature

Insurance Journal: California Smoke Damage Act Would Enable Wildfire Victims to Expedite Claims

California DOI: Nation’s First Smoke Damage Standards Bill — March 2026 Update

Congress.gov — S.2430: Wildfire Insurance Coverage Study Act of 2025